Greetings!

I am an applied macroeconomist studying international economics and macro-finance, with a focus on how global financial markets interact with domestic monetary policy through financial frictions and institutional design. I specialize in using applied macro-econometric methods—including LP, VAR, IV, DiD, and Bayesian analysis—to study sovereign debt markets, inflation-target credibility, and exchange rate puzzles. My job market paper uses a shift-share design—interacting endogenous currency shares with exogenous monetary shocks—to causally estimate the costs of sovereign defaults, finding sizable but temporary impacts. My research prepares me to teach courses in macroeconomics, money and banking, international finance, and time-series/financial forecasts.

I am a committed instructor who seeks to make economics accessible through historically grounded examples that speak to students from diverse backgrounds. I am deeply invested in undergraduate research mentorship and enjoy working closely with students through research assistantships. I look forward to supervising senior theses and supporting student participation in data-intensive projects (e.g., College Fed Challenge). I lead the "Global Price Initiative," which constructs time-geography-product price datasets from historical newspaper advertisements. Through both my teaching and research, I aim to integrate hands-on training in big data analysis, cloud computing, and applied AI tools while helping students prepare for both research careers and data-intensive roles in finance and consulting.

Research Interests: Macro, International Finance, and Applied Econometrics

Materials: CV • Research Statement • Teaching Statement • Teaching Evaluation

Update (03/12): I have posted a new working paper, Term Structure, Interest Volatility, and the Failure of the UIP Condition. A short non-technical summary is available here.

Update (01/19): I have posted a new working paper, Evaluating Emerging Markets' Monetary Policy. A short non-technical summary is available here.

Job Market Paper

Monetary Shocks, Currency Exposures, and the Cost of Sovereign Default

[Show/hide abstract] •

[Show/hide key results] •

[Non-technical summary]

[Current draft (November 2025)]

How costly is sovereign default? I develop a probabilistic sovereign default model that features (i) foreign monetary shocks induce self-fulfilling default equilibria; (ii) multiple equilibria imply a local average treatment effect; and (iii) under Fréchet heterogeneity in nominal exchange rates, default probability admits a shift-share form. Guided by these insights, I exploit aggregate variation in developing countries' currency denomination of external debt (endogenous shares) and advanced economies' quasi-random interest rate movements (exogenous shifts) to construct a shift-share instrumental variable (SSIV) for sovereign default decisions. Using a local projection–instrumental variable (LP-IV) approach, I causally estimate that sovereign defaults on average result in an 8% decline in real GDP per capita in the first year. The impact peaks at 18.5% around the second year, persists until the fourth year, and then fades toward zero by the sixth year. Moreover, I find that floating exchange rate regimes and lower external debt levels, especially short-term debt, effectively attenuate the output loss. Narrative monetary shocks and difference-in-difference analyses yield similar results, further confirming that sovereign default is indeed costly.

Working Papers

(New!) Term Structure, Interest Volatility,

and the Failure of the UIP Condition

[Show/hide abstract] •

[Show/hide key results] •

[Non-technical summary]

[Current draft (March 2026)]

The uncovered interest parity (UIP) condition predicts that the higher-interest-rate currency should depreciate so as to equalize expected returns across currencies. Yet despite its central role in international macro models, this condition is often rejected in the empirical data. This paper argues that UIP coefficient estimates are inherently regime-dependent, a latent feature that becomes visible once one studies their term structure. Using historical Eurocurrency/LIBOR deposit rates at the 1-, 3-, 6-, and 12-month maturities, I document three empirical facts. First, rolling-window UIP coefficient estimates are negatively related to the volatility of interest rate differentials, and this monotonic relationship evolves gradually over time rather than shifting discretely around the 2008 Global Financial Crisis. Second, both the sign and the magnitude of UIP coefficients vary across maturities: under normal times, short-maturity currency trades earn larger premia in high-volatility states, whereas near the zero lower bound the premium shifts toward longer-maturity deposits. Third, these maturity patterns are difficult to reconcile with a pure ``delayed-overshooting'' explanation based solely on sluggish exchange rate responses to monetary shocks, but they are also hard to explain using a standard finance-based ``risk premium'' argument alone. Instead, the term-structure evidence from UIP regressions points to the coexistence of both mechanisms, with time-varying risk premia---shaped in part by the signs of yield curve slopes---playing a central role in the UIP puzzle.

(New!) Evaluating Emerging Markets' Monetary

Policy

[Show/hide abstract] •

[Show/hide key results] •

[Non-technical summary]

[Current draft (January 2026)]

Are emerging markets' central banks credibly committed to inflation targeting? This paper applies the ``Optimal Policy Perturbation'' (OPP) framework of Barnichon and Mesters (2023) to evaluate monetary policy credibility across emerging economies. Combining impulse responses from a Bayesian VAR with professional forecasts from the Economist Intelligence Unit, I exploit the dual interpretation of the OPP statistic. First, under the assumption that observed policy rates are locally optimal given policymakers' information sets, I adopt a revealed-preference approach and recover time-varying implicit policy weights by minimizing deviations of the OPP statistic from zero. Second, under fixed benchmark weights, I use the OPP statistic to assess whether policy rates could have been adjusted to further reduce the policymaker's loss, and to quantify the direction and magnitude of such adjustments. The evidence indicates that inflation-target regimes in emerging markets have become increasingly credible since the early 2000s, with stronger anchoring of inflation expectations and reduced inflation persistence. While central banks face sharper trade-offs during global crises, monetary policy behavior typically reverts toward inflation stabilization, highlighting the flexibility and resilience of modern inflation-target frameworks.

Work in Progress

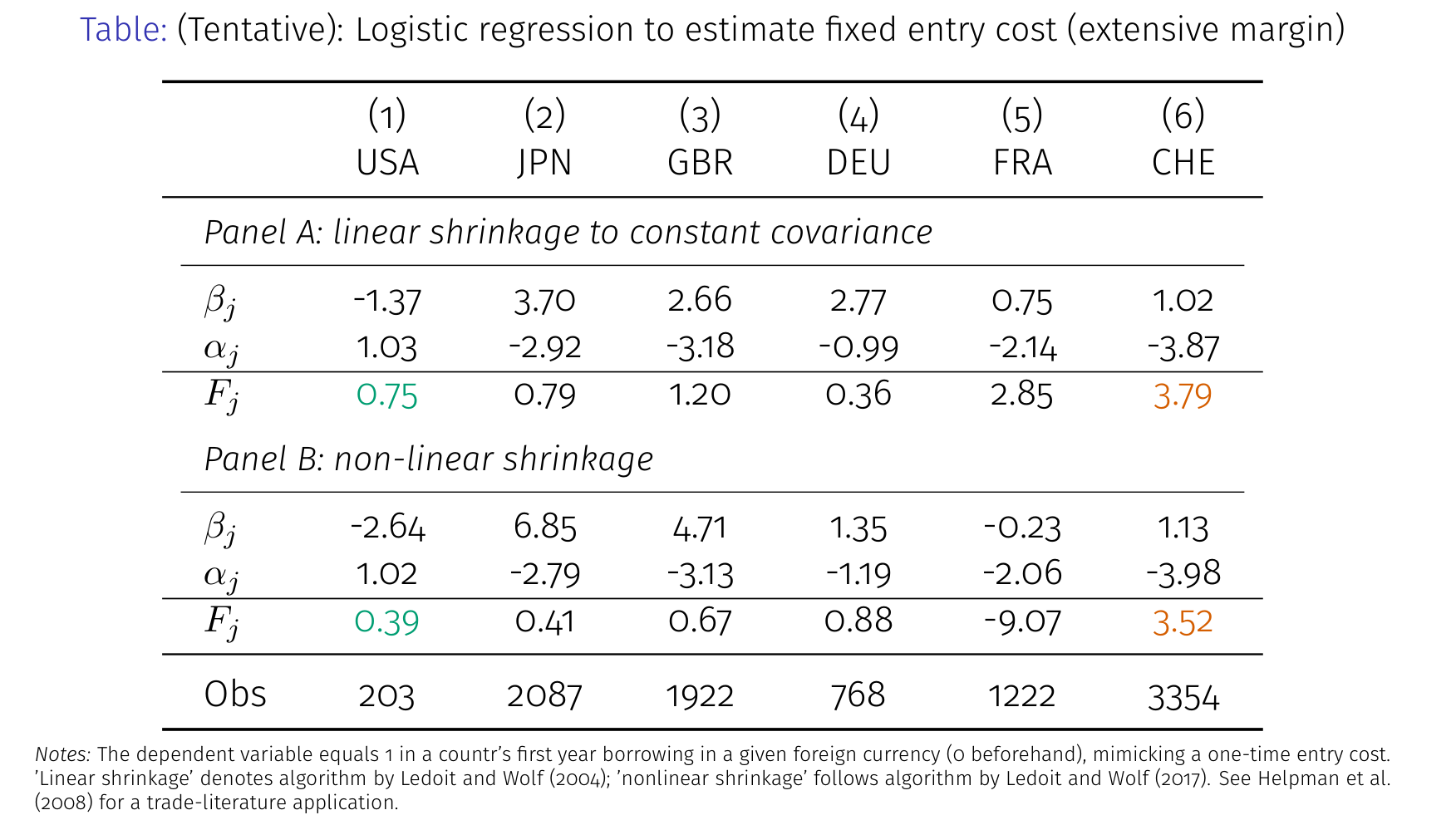

Currency Denomination of External Debts

[Show/hide abstract] •

[Show/hide key results]

Why do developing countries borrow predominantly in foreign currency rather than domestic currency (i.e., the "original sin")? Why is most external debt denominated in the U.S. dollar rather than other advanced economies' currencies? Since the currency denomination shapes emerging markets' balance-sheet exposure to the hegemon's monetary spillovers, understanding its determinants has direct policy implications for debt sustainability and financial market stability. This paper brings the trade literature—the Melitz (2003) model and Eaton-Kortum (2002) model—to bear on whether models that explain bilateral trade flows also account for the currency denomination of external debt. To rationalize the empirical fact that most external debt is denominated in U.S. dollar, I introduce non-negligible fixed entry costs of borrowing in an additional currency. From a finance perspective, I also incorporate an optimal portfolio choice model to assess consistency with the trade mechanism. The key insights highlight the importance of trade frictions in the international borrowing markets, which include (i) the fixed-cost margin generates threshold behavior in currency adoption (extensive margin), and (ii) the heterogeneous creditors generate strategic complementarities, so small cost-push shocks need not necessarily overturn currency denomination shares.

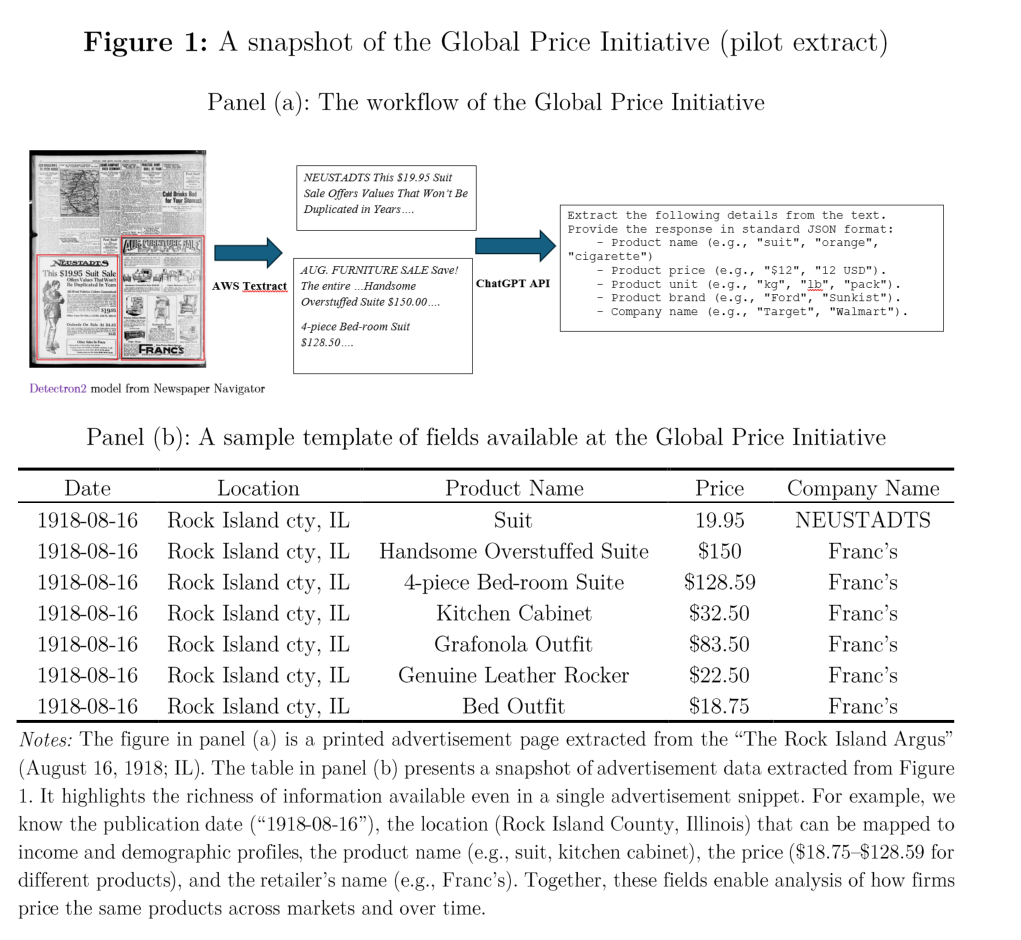

The Price of Everything Everywhere

[Show/hide abstract] •

[Show/hide key results] •

[Non-technical summary]

[Preliminary draft (October 2025)]

This research project develops a novel historical dataset on prices of tradable goods and non-tradable services (occupation-level wages), returns on financial assets (bank deposit rates across maturities), as well as firms' balance sheets, across U.S. counties and international borders from 1850 to 2000. Using advanced machine learning methods, I examine printed advertisements from millions of digitized historical newspapers in order to shed light on (i) price stickiness and firms' markup structures at both domestic and international scales, (ii) the heterogeneous and distributional effects of macroeconomic policies—such as tariffs and monetary shocks—on realized inflation experienced by households from different income groups and demographic compositions across geographies, and (iii) the differential factor prices for capital and labor (e.g., interest/mortgage rates across maturities, and offered wages across service occupations) in different regions. The resulting “Global Price Initiative” database provides researchers with a highly detailed, product-level dataset that supports transparency, replicability, and versatility in macroeconomic and international research on prices.

Publications

Zombie lending, labor hoarding, and local industry growth

with Masami Imai (Wesleyan University)

Japan and the World Economy, Volume 71, (September 2024)

[Show/hide abstract]

[Published version]

After the bursting of real estate bubbles in 1991, Japanese banks continued lending to unviable firms to conceal problem loans. We revisit Japan's experience and propose a new mechanism via which banks' loan-evergreening policy undermines allocative efficiency across industries by focusing on construction and real estate loans. Namely, banks' continuing support for construction and real estate firms encourages labor hoarding in unviable construction projects. Since construction projects predominantly use low-skilled workers, banks' loan-evergreening policy in these troubled sectors may depress other low-skilled industries. Based on the industry-level data in each of Japan's 47 prefectures from 1992 to 1996, we document empirical facts consistent with this hypothesis. On average, low-skilled industries experienced disproportionately slower output and employment growth and more sluggish growth in the number of new establishments in prefectures where the share of bank loans to local construction/real estate sectors increased more after construction boom ended.